Chapter 12 Terms and Notes:

| Assignments | |||

Terms:

Board of Directors: A group of persons elected by the stockholders to manage a corporation.

Articles of Incorporation: A written applications requesting permission to form a corporation.

Charter: The approved articles of incorporation.

Common Stock: Stock that does not give stockholders any special preferences.

Preferred Stock: Stock that gives stockholders preference in earnings and other rights.

Stock Certificate: Written evidence of the number of shares each stockholder owns in a corporation.

Par Value: A share of stock that has an authorized value printed on the stock certificate.

No-Par-Value Stock: A share of stock that has not authorized value printed on the stock certificate.

Stated-Value Stock: No-par-value stock that is assigned a value by a corporation.

Subscribing for Capital Stock: Entering into an agreement with a corporation to buy capital stock and pay at a later date.

Organization Costs: Fees and other expenses of organizing a corporation.

Intangible Assets: Assets of a non-physical nature that have value for a business.

Declaring a Dividend: Action by a board of directors votes to distribute a dividend.

Date of Declaration: The date on which a board of directors votes to distribute a dividend.

Date of Record: The date that determines which stockholders are to receive dividends.

Date of Payment: The date on which dividends are actually to be paid to the stockholders.

Remember your account classifications:

Balance Sheet Accounts:

(1000) Assets with 1100 Current Assets 1200 Long-Term Investment, 1300 Plant Assets, 1400 Intangible Assets.

(2000) Liabilities with 2100 Current Liabilities, 2200 Long-Term Liabilities.

(3000) Stockholders Equity

Income Statement Accounts:

(4000) Operating Revenue

(5000) Cost of Merchandise

(6000) Operating Expenses with 6100 Selling Expenses,6200 Administrative Expenses.

(7000) Other Revenue

(8000) Other Expense

(9000) Income Tax

Corporate Business Form

Nature of a Corporation

A corporation exists as a separate entity. It can sue and be sued and the corporation is viewed the same a person. Each unit of ownership in a corporation is called a share. The total shares of a corporation are known as capital stock. The corporate earnings given to owners are called dividends are shared by the owners of the business known as shareholders or stockholders.

Legal Requirements

In order to start the process individuals must submit an application to the appropriate officials in the state the corporation will be in. This is known as the articles of incorporation. When the application is approved a charter also known as a certificate of incorporation will be given to the corporation

Rights Possessed by Shareholders

The right to vote unless restricted by type of stock.

The right to share in profits.

The right share in distribution of liquidated assets.

Types and Characteristics of Stock

Common--no special preferences---voting rights

Preferred--preference to earnings---no voting rights

Cumulative--dividends accrue from year to year if not paid

Participating--dividends given after preferred paid and

common paid, then all share dividends.

Par-Value Stock--Value assigned and printed on stock.

No-Par Value Stock--No authorized value printed on the stock

Stated Value Stock--No par value with assigned value but not printed on stock.

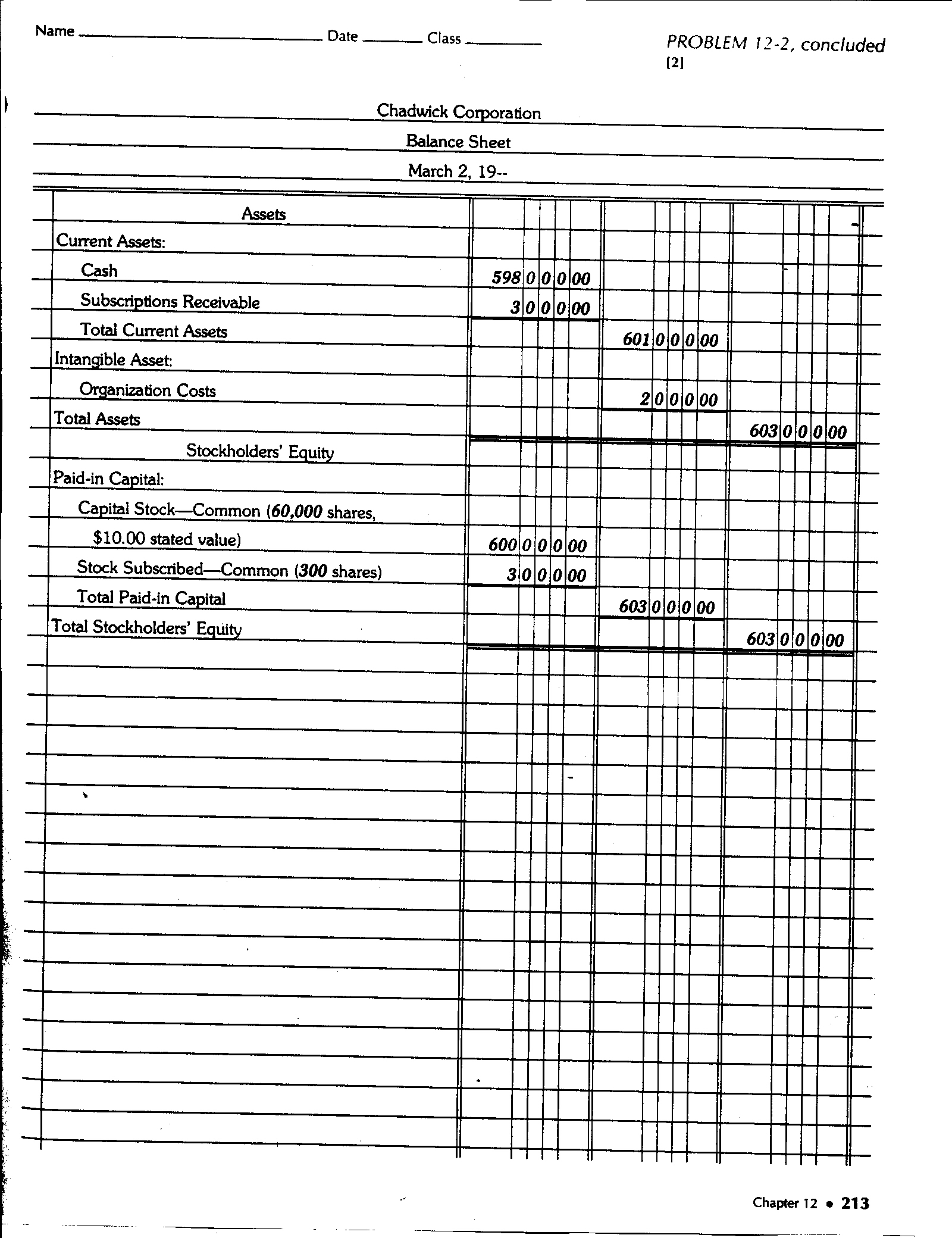

Capital Accounts in a Corporation

Retained Earnings--Normal Credit Balance. Capital account designed to hold corporate earnings.

Capital Stock---Normal Credit Balance. Capital account designed to hold money invested in the business.

Capital Stock-Common

Capital Stock-Preferred

Treasury Stock--Normal Debit Balance. Capital account designed to hold amount for issued stock purchased by the corporation.

Dividends---Normal Debit Balance. Consider it like a drawing account in

partnerships/proprietorships. Accounts used to hold corporate profits

being distributed to sharelholders.

Dividends-Common

Dividends-Preferred

Income Summary---Can have a Debit or Credit Balance. Treated the same

as in proprietorship/partnerships.

Other Stockholder's Accounts:

Stock Subscribed-Common

Paid-in Capital in Excess of Stated

Value-Common

Stock Subscribed-Preferred

Paid-in Capital in Excess of Par

Value-Preferred

Discount on Sale of Preferred Stock

Paid- in Capital from Sale of

Treasury Stock

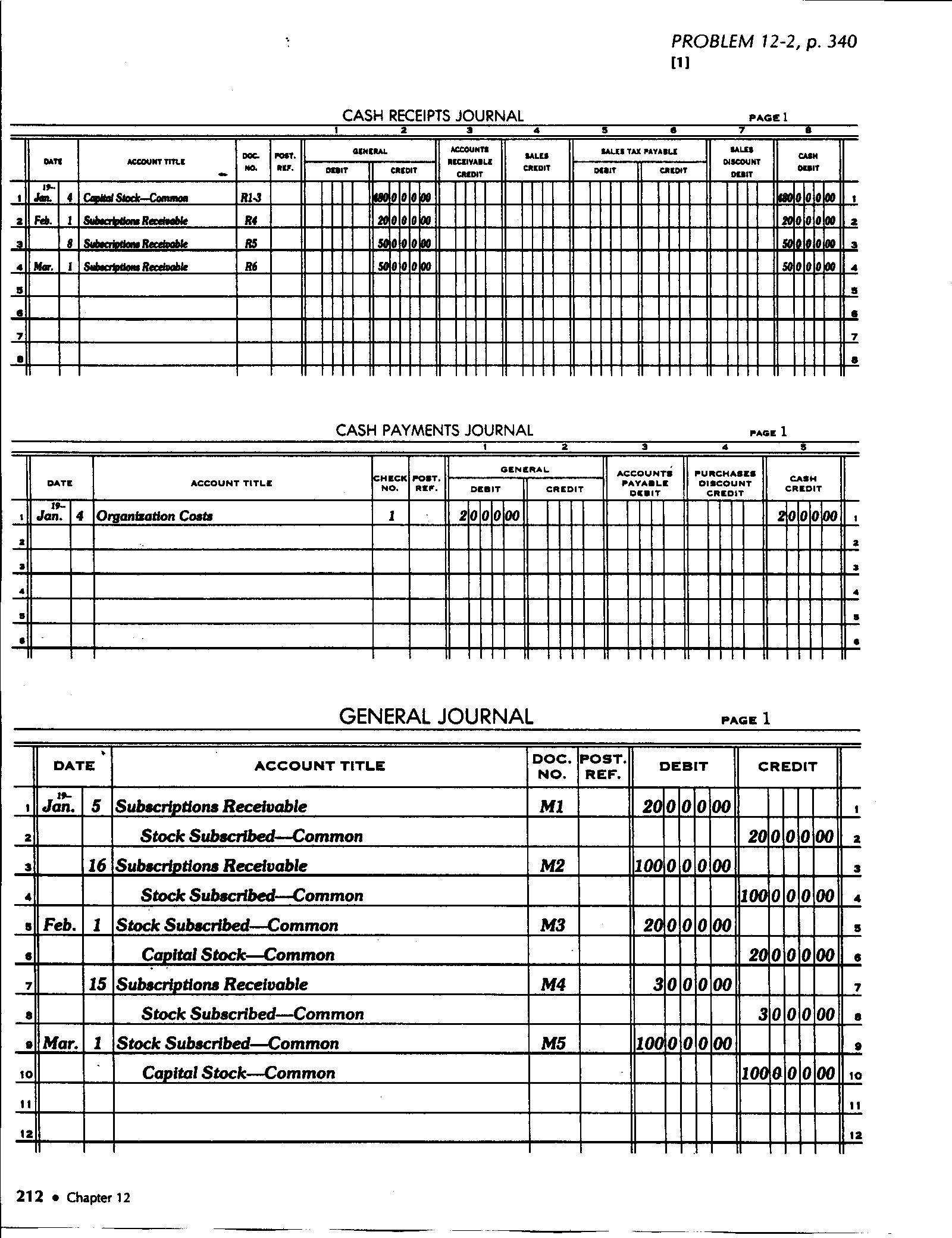

Transactions involving Capital Stock:

1. Issuing Capital Stock When Forming a Corporation:

Received cash from six incorporators for 30,000 shares of $10.00 stated-value common stock, $300,000. Receipt No. 1-6.

In the cash receipts journal: Cash Debit---Capital Stock-Common Credit

2. Subscribing for Capital Stock:

Received a subscription from Doug Kranz for 2,000 shares of $10.00 stated-value common stock, $20,000.00. Memorandum No. 1.

In the general journal: Subscriptions Receivable Debit----Stock Subscribed--Common Credit.

3. Cash Receipt of Subscribed Stock:

Received cash from Doug Kranz in partial payment of stock subscription, $10,000.00. Receipt No. 4

In the cash receipts journal: Subscriptions Receivable general credit---Cash debit.

4. Issuance of Stock Previously Subscribed:

Issued Stock Certificate No. 7 to Doug Kranz for 2,000 shares of $10.00 stated-value common stock. Memorandum.67.

In the General Journal debit Stock Subscribed-Common--credit Capital Stock-Common.

Organization Costs:

Organization Costs may include: an incorporation fee paid to the state for charter application, attorney fees for legal services during the process of incorporation, other incidental costs incurred prior to receipt of the charters.

Usually these costs are paid by one of the incorporators until the charter is granted. After the charter is obtained an individual will be reimbursed by the corporation. These costs are recorded as an asset. To record organization costs do so in the cash payments journal crediting cash and organizational costs general debit.

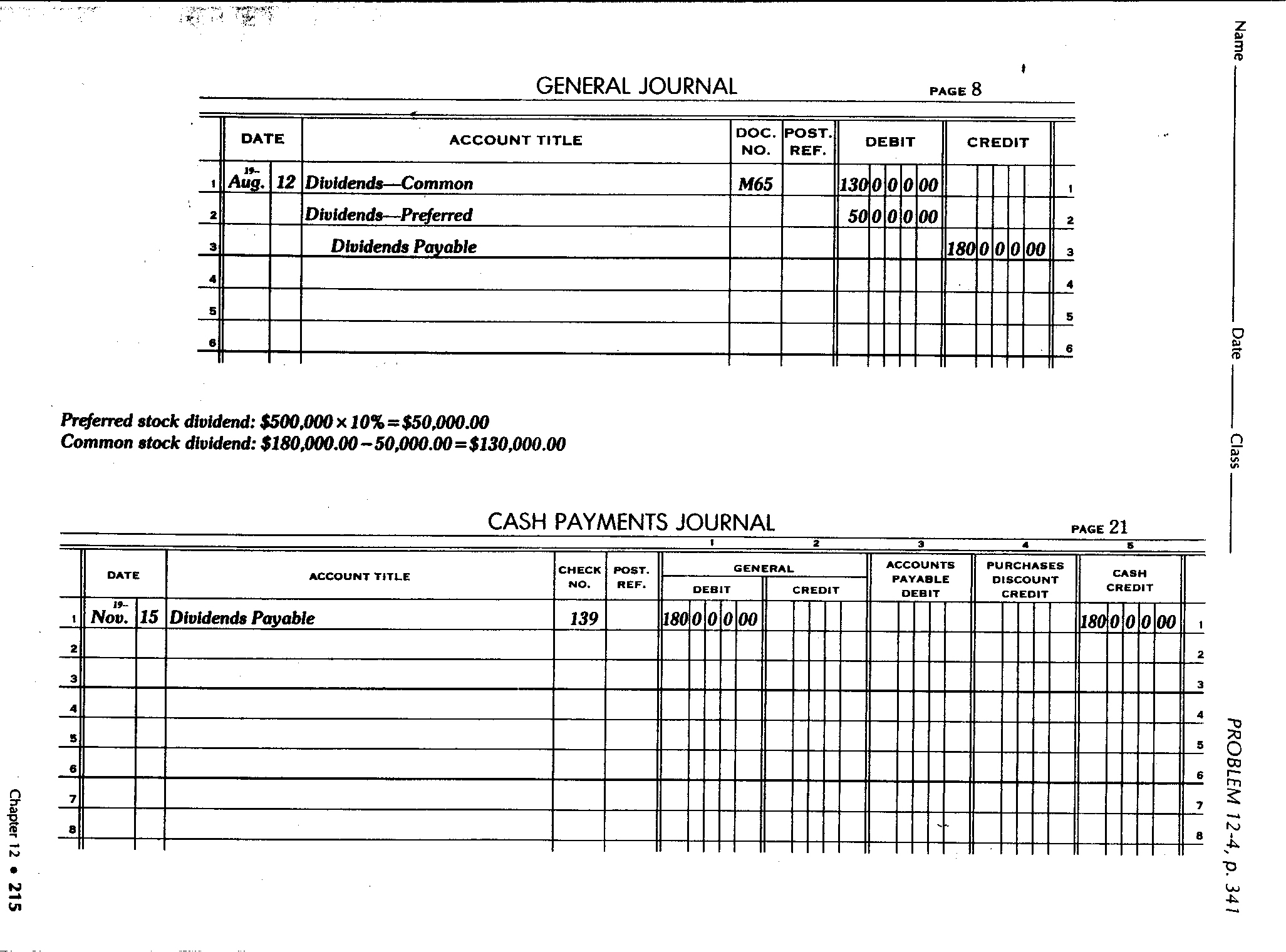

Dividends:

Three important dates are noted for dividends

1. Date of Declaration. The date the board of directors declares there will be payment. Transaction to be recorded in the general journal is Dividends Debit and Dividends Payable credit.

2. Date of Record. The date that determines which stockholders receive dividends. You my buy and sell stocks but only those holding the stocks on the day of record will receive dividends. No transaction with this step.

3. Date of Payment. Day on which dividends are actually paid. Transaction to be recorded involves Dividends Payable debit and Cash credit in the cash payments journal.

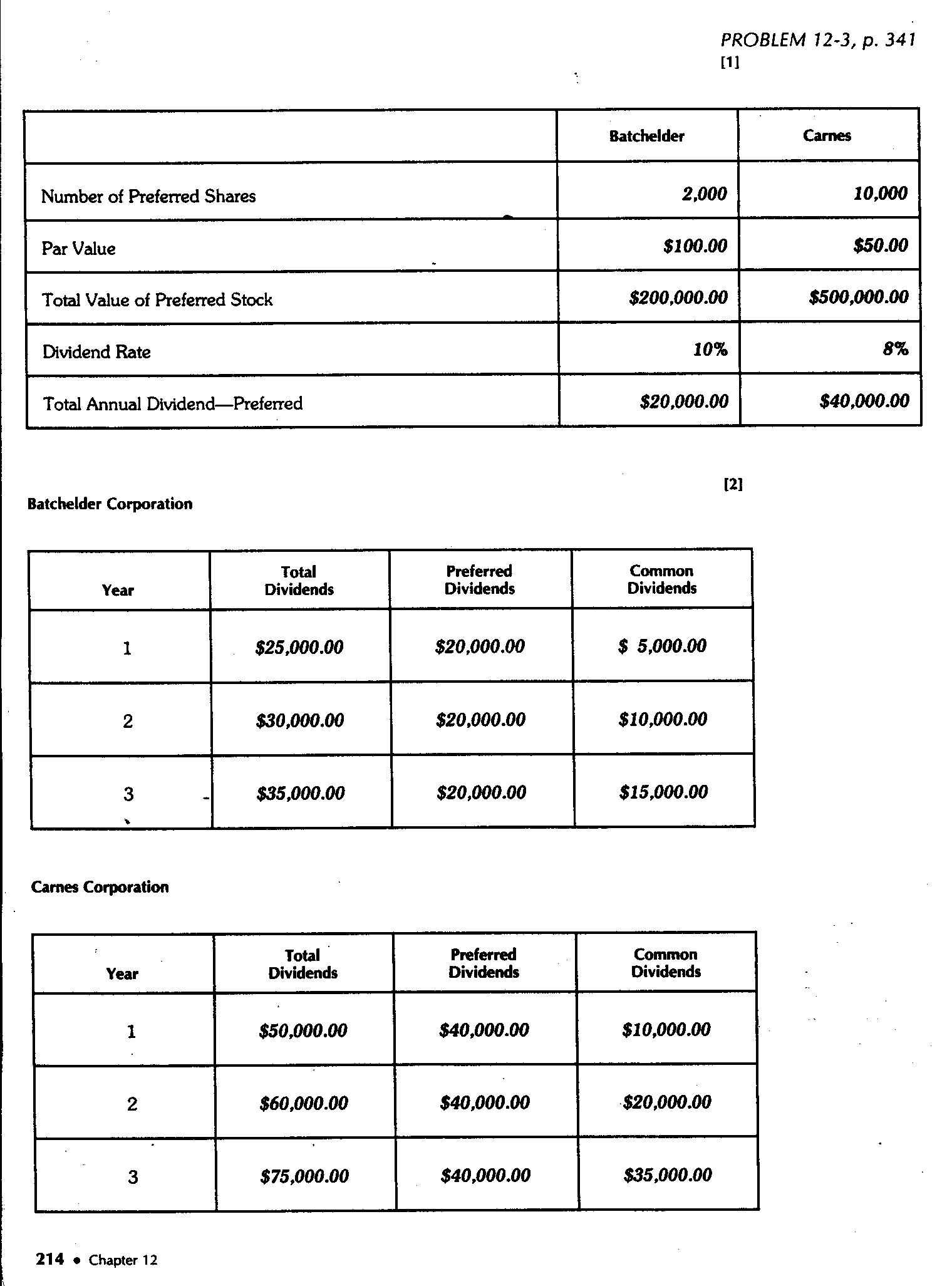

Steps To Calculate Dividends:

1. Number of Shares X Value =Value of Stock

2. Value of Stock X Dividend Rate = Dividend Amount

3. Total Amount available for Dividends - Preferred Dividend Amount = Common Dividend Amount.

4. Common Dividend Amount divided by Value of Common Stock = Common Dividend Rate.

Assignments to be completed for this Chapter:

Some assignments will be done together and others on your own. If you have trouble viewing or are absent solutions to the joint projects are available for you.

Joint Class Projects:

Day 1 & 2: Presentation & Problems 12-1 Solution, 12-2,Solution Pg1, Solution Pg2, 12-3, Solution,12-4 Solution. Assignment outside class to read Chapter 12.

Individual Projects:

Day 3 & 4: Problem 12-M, 12-C.

Questions for individual study which will be discussed in class.

Day 5: Study Guide 12 and Problem Test 12 will be delivered for

class.

Day 6: Assessment follow-up. Understanding Check-up.

Click here

to do Case Study #1 & #2:

Day 7: You have this day and will need to be ready to present one week from today. Create a power point presentation at each site to to address the following: 1. Prepare a list of skills learned in accounting that can be used in everyday life. 2. Elaborate by writing or orally discussing each skill and how it is advantageous to gain this skill.

| Assignments | |||

{kind=link}

{kind=link}

{kind=link}

{kind=link}